Chips: Advanced packaging blijft in de picture staan

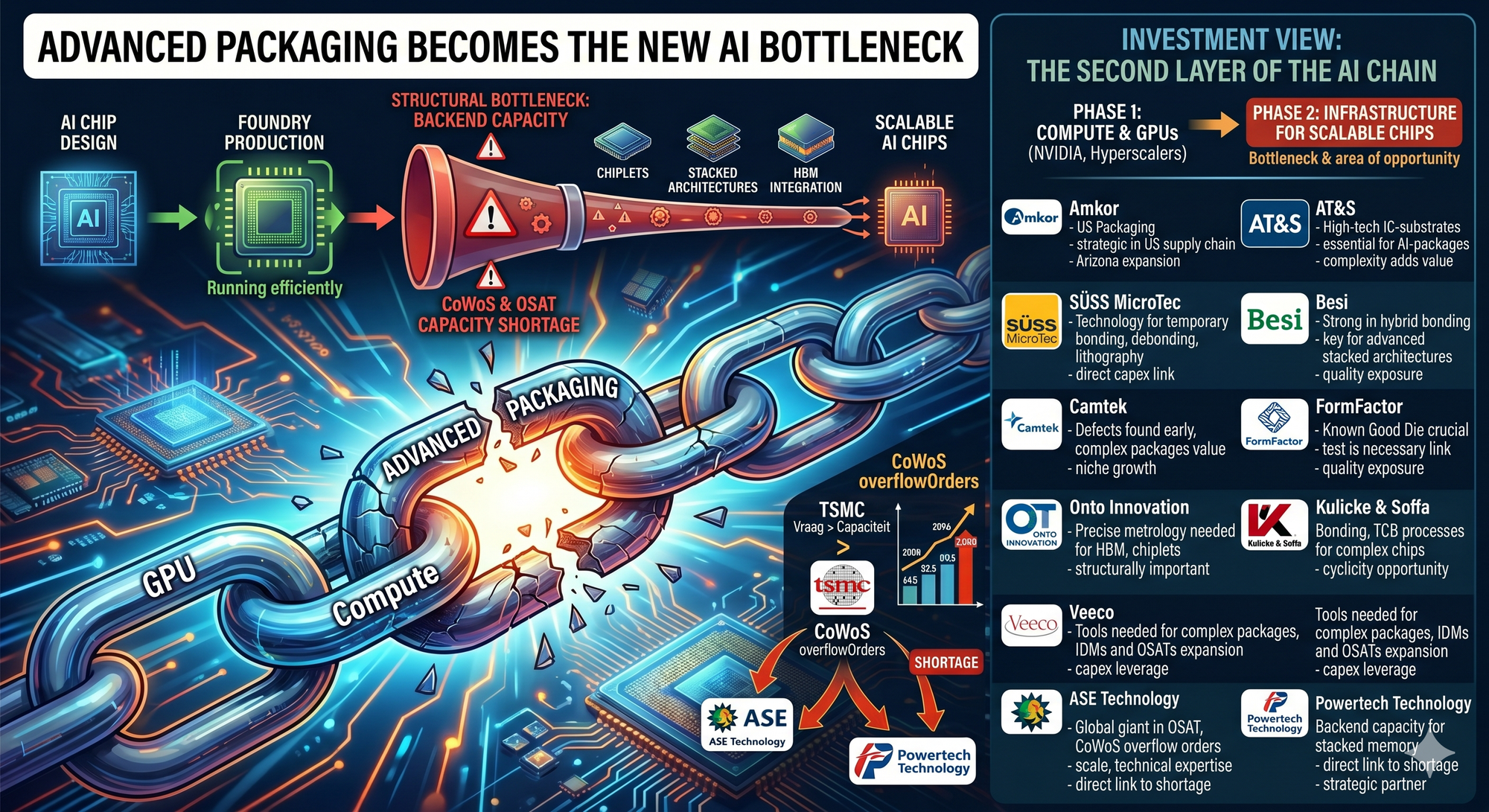

De AI-markt draait al lang niet meer alleen om GPU’s. Wij besteden hier al langere tijd aandacht aan, omdat de druk in de keten steeds nadrukkelijker verschuift naar advanced packaging, CoWoS-capaciteit, chiplets, HBM-integratie, substrates, test en metrologie. Dat beeld wordt nu sterker bevestigd. Zelfs de krachtigste AI-chip heeft weinig waarde als de packagingcapaciteit niet snel genoeg meegroeit.

De berichten dat TSMC niet aan alle CoWoS-vraag kan voldoen en dat overflow-orders richting partijen als ASE en Powertech gaan, maken concreter wat wij al langer denken. De backend van de halfgeleiderketen wordt een structureel knelpunt in de AI-cyclus. De meeste aandacht gaat nog altijd naar de grote AI-chipnamen, maar de echte hefboom kan de komende fase juist liggen bij bedrijven die deze chips schaalbaar maken: specialisten in advanced packaging, substrates, bonding, test en metrologie.

Investment view

Wij kijken positief naar de tweede laag van de AI-keten. De eerste fase van de AI-rally draaide vooral om compute, GPU’s en hyperscalers. De volgende fase kan veel meer gaan draaien om de infrastructuur die nodig is om die chips op grote schaal bruikbaar te maken. Daar zit de bottleneck. Niet in de belofte van AI, maar in de fysieke capaciteit om complexe chips te bouwen, te verbinden, te testen en te verpakken.

■ Advanced packaging wordt een structurele schakel in AI.

■ CoWoS-capaciteit blijft krap door de vraag naar AI-chips.

■ Overflow-orders richting ASE en Powertech bevestigen de druk in de backend.

■ Substrates, bonding, test en metrologie krijgen een grotere strategische rol.

■ De beste hefboom ligt bij bedrijven die de AI-keten schaalbaar maken.

Dat is voor beleggers belangrijk. Een bottleneck trekt investeringen aan. Wanneer TSMC onvoldoende CoWoS-capaciteit heeft, ontstaat ruimte voor OSAT’s, substrateproducenten, bonding-specialisten, testbedrijven en metrologiespelers. Dit zijn niet altijd de namen die bovenaan de AI-lijstjes staan, maar ze zitten wel op een plek waar extra capex direct kan doorwerken in orders, omzet en waardering.

De upside verschilt per aandeel. Directe packagingbedrijven zoals Amkor, ASE en Powertech hebben de duidelijkste link met de capaciteitskrapte. Europese namen zoals AT&S, SÜSS MicroTec en Besi bieden blootstelling aan substrates, bonding en equipment. Aan de Amerikaanse kant zijn Camtek, FormFactor, Onto Innovation, Kulicke & Soffa en Veeco interessant als tweede-laags AI-spelers met specifieke blootstelling aan inspectie, test en advanced packaging tools.

Amkor Technology $AMKR

Amkor is waarschijnlijk de meest directe Amerikaanse beursgenoteerde naam binnen dit thema. Het bedrijf zit in outsourced semiconductor packaging and test en wordt relevanter naarmate chipbedrijven meer capaciteit buiten de traditionele Aziatische keten willen veiligstellen.

De upside kan stevig zijn als de markt Amkor niet langer alleen ziet als een cyclische OSAT, maar als een strategische infrastructuurspeler binnen AI. De samenwerking met grote chipbedrijven en de uitbreiding in Arizona maken het bedrijf belangrijker in de Amerikaanse halfgeleiderketen. Dat kan tot een hogere waardering leiden wanneer beleggers meer gewicht geven aan advanced packaging.

Het risico blijft dat packaging marges kent die lager kunnen liggen dan bij pure equipmentbedrijven. Toch is Amkor binnen de Verenigde Staten één van de zuiverste manieren om in te spelen op de groei van advanced packaging.

AT&S $ATS

AT&S is een Europese naam die veel beter past binnen het AI-thema dan de markt soms erkent. Het bedrijf zit in hoogwaardige IC-substrates. Die zijn essentieel voor AI-packages, omdat de verbinding tussen chips, geheugen en andere componenten steeds complexer wordt.

De upside kan groot zijn als beleggers AT&S meer gaan waarderen als AI-substrate-speler. Substrates zijn kapitaalintensief en technisch veeleisend. Dat maakt de markt niet eenvoudig, maar juist daardoor kan krapte in hoogwaardige capaciteit waarde creëren voor bedrijven die goed gepositioneerd zijn.

AT&S heeft een hoger risicoprofiel door de grote investeringen die nodig zijn. Als de vraag naar AI-substrates echter sterk blijft, kan het aandeel profiteren van een duidelijke herwaardering.

SÜSS MicroTec $SMHN

SÜSS MicroTec is een kleinere Duitse equipmentnaam met blootstelling aan advanced backend-processen. Het bedrijf levert technologie voor onder meer temporary bonding, debonding, lithografie en bonding-systemen.

De upside kan bovengemiddeld zijn omdat SÜSS kleiner is en gevoeliger reageert op ordergroei. Wanneer OSAT’s, foundries en IDM’s hun advanced packagingcapaciteit uitbreiden, moeten zij investeren in tools die deze processen mogelijk maken. Daar zit de directe link met de AI-capexcyclus.

Het aandeel kan volatiel blijven, omdat kleinere semicapnamen hard bewegen op orders en verwachtingen. Toch is de positionering sterk. SÜSS zit op een plek waar meer complexiteit in chips rechtstreeks leidt tot meer behoefte aan gespecialiseerde equipment.

BE Semiconductor Industries $BESI

Besi blijft één van de sterkste Europese namen binnen advanced packaging. Het bedrijf is vooral relevant door hybrid bonding, een technologie die belangrijker wordt bij chiplets, gestapelde architecturen en complexere AI-chips.

De upside is nog steeds aanwezig, maar Besi is al beter ontdekt door de markt. Daardoor is het aandeel minder verborgen dan sommige andere namen in dit overzicht. De kwaliteit van de exposure blijft echter hoog. Als hybrid bonding sneller doorbreekt, kan Besi opnieuw profiteren van een nieuwe investeringsronde.

Voor beleggers is Besi vooral een kwaliteitsnaam binnen dit thema. Niet de meest onbekende speler, wel één van de technologisch sterkere bedrijven in Europa.

Camtek $CAMT

Camtek is interessant omdat inspectie en metrologie steeds belangrijker worden bij advanced packaging. Hoe duurder en complexer een AI-package wordt, hoe groter de noodzaak om defecten vroeg in het proces te vinden.

De upside kan sterk zijn door de combinatie van nichepositie en structurele vraaggroei. Camtek profiteert niet alleen van meer volume, maar vooral van hogere complexiteit. Bij AI-packages met HBM en chiplets neemt de waarde van betrouwbare inspectie toe.

Het aandeel kan gevoelig zijn voor waardering, maar de strategische positie is aantrekkelijk. Camtek is een duidelijke tweede-laags AI-naam die veel beleggers minder snel noemen dan de grote chipbedrijven.

FormFactor $FORM

FormFactor past goed in dit thema door zijn rol in wafer-level test en probe-technologie. Bij AI-chips wordt known good die steeds belangrijker. Fabrikanten willen defecte onderdelen uitsluiten voordat ze in een duur package terechtkomen.

De upside zit in de herwaardering van test als noodzakelijke schakel in AI-productie. FormFactor is geen pure hype-naam, maar de relevantie neemt toe wanneer HBM, chiplets en 2.5D- of 3D-packaging belangrijker worden.

Het aandeel lijkt minder explosief dan sommige kleinere nichebedrijven, maar de kwaliteit van de blootstelling is degelijk. Voor beleggers die een minder speculatieve route zoeken binnen de tweede laag van AI, is FormFactor interessant.

Onto Innovation $ONTO

Onto Innovation is een bredere speler in process control en metrologie. Het bedrijf profiteert van de toenemende precisie die nodig is bij heterogeneous integration, advanced packaging en nieuwe substrate-technologieën.

De upside is vooral aantrekkelijk wanneer advanced packaging uitgroeit tot een meerjarige investeringscyclus. Complexere chips vragen meer meetpunten, betere controle en hogere yield. Dat maakt metrologie structureel belangrijker.

Onto is minder puur dan sommige andere namen, maar de breedte maakt het aandeel juist robuuster. Het is een kwaliteitsnaam binnen het bredere advanced packaging-ecosysteem.

Kulicke & Soffa $KLIC

Kulicke & Soffa is een kleinere assembly-equipmentnaam. Het bedrijf krijgt blootstelling aan bonding, thermocompression bonding en andere processen die belangrijker worden naarmate chiparchitecturen complexer worden.

De upside kan bovengemiddeld zijn als advanced packaging-capex versnelt. KLIC is cyclisch, maar juist daardoor kan het aandeel hard reageren wanneer orders verbeteren en beleggers de backend van de chipketen opnieuw waarderen.

Het risico is dat de ordercyclus grillig blijft. Toch past KLIC goed in het thema. Het bedrijf zit niet bovenaan het AI-verhaal, maar levert wel technologie die nodig is om de volgende fase van packaging mogelijk te maken.

Veeco $VECO

Veeco is een kleinere Amerikaanse equipmentnaam met blootstelling aan advanced packaging lithography. Het bedrijf is geen pure CoWoS-play, maar wel relevant voor capaciteitsexpansies bij IDM’s en OSAT’s.

De upside zit in de mogelijkheid dat beleggers dieper in de AI-supplychain gaan zoeken. Veeco krijgt minder aandacht dan de grote semicapnamen, maar gespecialiseerde tools blijven nodig wanneer de backend complexer wordt.

De case is indirecter dan bij Amkor of Camtek, maar daardoor kan het aandeel verrassen als de markt het thema breder oppakt. Binnen een sterke capexcyclus kan Veeco een duidelijke equipmenthefboom bieden.

ASE Technology $ASX

ASE is één van de belangrijkste bedrijven ter wereld in outsourced semiconductor assembly and test. Als TSMC onvoldoende CoWoS-capaciteit heeft, ligt het voor de hand dat ASE meer aandacht krijgt van klanten die extra advanced packagingcapaciteit zoeken.

De upside is fundamenteel sterk door schaal, technische expertise en directe blootstelling aan packaging. ASE is wel bekender dan kleinere nichebedrijven, waardoor de kans op een extreme herwaardering kleiner kan zijn. De strategische relevantie blijft echter zeer hoog.

ASE is vooral een kernnaam om de kracht van de advanced packaging-cyclus te volgen. Als de vraag hier blijft oplopen, bevestigt dat het bredere investeringsverhaal.

Powertech Technology

Powertech Technology is relevant omdat het direct wordt genoemd als mogelijke ontvanger van overflow-orders. Het bedrijf zit in assembly en test en heeft daardoor directe blootstelling aan backendcapaciteit.

De upside kan stevig zijn als beleggers gaan geloven dat deze orders onderdeel zijn van een structurele verschuiving. Powertech is minder bekend bij westerse beleggers, maar operationeel zit het dicht op de kern van het probleem.

De praktische toegankelijkheid van het aandeel kan beperkter zijn voor Europese en Amerikaanse beleggers. Thematisch hoort Powertech wel duidelijk in dit overzicht. Het bedrijf zit precies in de laag waar AI-capaciteit nu krap wordt.

Conclusie

De AI-cyclus wordt breder. GPU’s blijven belangrijk, maar de volgende bottleneck zit steeds duidelijker in advanced packaging, CoWoS-capaciteit, substrates, bonding, test en metrologie. Dat is precies het thema waar wij al langer aandacht aan besteden.

De berichten rond TSMC, ASE en Powertech maken de signalen sterker. De markt begint beter te zien dat AI niet alleen draait om de chip zelf, maar ook om de infrastructuur die nodig is om die chip op schaal te produceren en betrouwbaar te laten werken.

Onze voorkeur gaat uit naar bedrijven met directe blootstelling aan hogere packaging-capex en toenemende complexiteit. Amkor, AT&S, SÜSS MicroTec, Besi en Camtek springen er daarbij het meest uit. ASE en Powertech blijven belangrijke kernnamen binnen de directe packagingketen, terwijl FormFactor, Onto Innovation, Kulicke & Soffa en Veeco interessante tweede-laags spelers zijn.

Wij blijven positief over dit thema. De signalen worden sterker en de markt lijkt langzaam te bevestigen wat wij al langer denken: de echte AI-hefboom kan de komende fase juist liggen bij de bedrijven die de chipketen schaalbaar maken.

English version

Advanced packaging is becoming the next AI bottleneck

The AI market is no longer only about GPUs. We have been paying attention to this theme for some time, because pressure in the semiconductor chain is increasingly shifting toward advanced packaging, CoWoS capacity, chiplets, HBM integration, substrates, testing and metrology. That view is now being confirmed more clearly. Even the most powerful AI chip has limited value if packaging capacity cannot scale fast enough.

Reports that TSMC cannot fully meet CoWoS demand and that overflow orders are moving toward companies such as ASE and Powertech make the issue more concrete. The backend of the semiconductor chain is becoming a structural constraint in the AI cycle. Most market attention still goes to the large AI chip names, but the next phase of upside may sit with the companies that make those chips scalable: specialists in advanced packaging, substrates, bonding, testing and metrology.

Investment view

We are positive on the second layer of the AI chain. The first phase of the AI rally was mainly about compute, GPUs and hyperscalers. The next phase may increasingly focus on the infrastructure required to make those chips usable at scale. That is where the bottleneck sits. Not in the promise of AI, but in the physical capacity to build, connect, test and package complex chips.

For investors, this matters. Bottlenecks attract capital. When TSMC lacks sufficient CoWoS capacity, opportunities emerge for OSATs, substrate producers, bonding specialists, testing companies and metrology players. These are not always the names at the top of AI stock lists, but they are positioned where additional capex can flow directly into orders, revenue and valuation.

■ Advanced packaging is becoming a structural part of AI.

■ CoWoS capacity remains tight because of demand for AI chips.

■ Overflow orders toward ASE and Powertech confirm backend pressure.

■ Substrates, bonding, testing and metrology are becoming more strategic.

■ The best leverage sits with companies that make the AI chain scalable.

The upside differs by stock. Direct packaging companies such as Amkor, ASE and Powertech have the clearest link to capacity constraints. European names such as AT&S, SÜSS MicroTec and Besi provide exposure to substrates, bonding and equipment. In the United States, Camtek, FormFactor, Onto Innovation, Kulicke & Soffa and Veeco are interesting second-layer AI names with specific exposure to inspection, testing and advanced packaging tools.

Amkor Technology $AMKR

Amkor is probably the most direct listed US name within this theme. The company operates in outsourced semiconductor packaging and test and becomes more relevant as chip companies look to secure additional capacity outside the traditional Asian supply chain.

The upside can be strong if the market stops viewing Amkor only as a cyclical OSAT and starts valuing it as a strategic AI infrastructure player. Its partnerships with large chip companies and expansion in Arizona make the company more important in the US semiconductor chain. That can support a higher valuation if investors attach more value to advanced packaging.

The risk is that packaging margins can remain lower than those of pure equipment companies. Still, within the US market, Amkor is one of the cleanest ways to play the growth of advanced packaging.

AT&S $ATS

AT&S is a European name that fits the AI theme better than the market often recognizes. The company operates in high-end IC substrates. These are essential for AI packages, because the connection between chips, memory and other components is becoming increasingly complex.

The upside can be significant if investors start valuing AT&S more as an AI substrate player. Substrates are capital-intensive and technically demanding. That makes the market challenging, but it also means tight high-end capacity can create value for well-positioned companies.

AT&S carries a higher risk profile because of the large investments required. If demand for AI substrates remains strong, the stock can benefit from a clear re-rating.

SÜSS MicroTec $SMHN

SÜSS MicroTec is a smaller German equipment name with exposure to advanced backend processes. The company supplies technology for temporary bonding, debonding, lithography and bonding systems.

The upside can be above average because SÜSS is smaller and more sensitive to order growth. When OSATs, foundries and IDMs expand advanced packaging capacity, they need tools that enable these processes. That is the direct link with the AI capex cycle.

The stock can remain volatile, because smaller semiconductor equipment names often move sharply on orders and expectations. Still, the positioning is strong. SÜSS sits in an area where rising chip complexity creates direct demand for specialized equipment.

BE Semiconductor Industries $BESI

Besi remains one of the strongest European names in advanced packaging. The company is especially relevant through hybrid bonding, a technology that becomes more important for chiplets, stacked architectures and more complex AI chips.

The upside is still present, but Besi is already better recognized by the market. That makes the stock less hidden than some other names in this article. The quality of its exposure remains high. If hybrid bonding adoption accelerates, Besi can benefit from another investment cycle.

For investors, Besi is mainly a quality name within this theme. Not the most undiscovered player, but one of the stronger technology companies in Europe.

Camtek $CAMT

Camtek is interesting because inspection and metrology are becoming more important in advanced packaging. The more expensive and complex an AI package becomes, the greater the need to detect defects early in the process.

The upside can be strong because of the combination of niche positioning and structural demand growth. Camtek benefits not only from higher volume, but also from rising complexity. In AI packages with HBM and chiplets, the value of reliable inspection increases.

The stock can be valuation-sensitive, but the strategic position is attractive. Camtek is a clear second-layer AI name that many investors mention less often than the large chip companies.

FormFactor $FORM

FormFactor fits well within this theme through its role in wafer-level test and probe technology. With AI chips, known good die becomes increasingly important. Manufacturers want to exclude defective components before they enter an expensive package.

The upside lies in the revaluation of test as a necessary part of AI production. FormFactor is not a pure hype name, but its relevance increases as HBM, chiplets and 2.5D or 3D packaging become more important.

The stock is likely less explosive than some smaller niche companies, but the quality of exposure is solid. For investors looking for a less speculative route into the second layer of AI, FormFactor is interesting.

Onto Innovation $ONTO

Onto Innovation is a broader process control and metrology company. It benefits from the rising precision required in heterogeneous integration, advanced packaging and new substrate technologies.

The upside is especially attractive if advanced packaging becomes a multi-year investment cycle. More complex chips require more measurement points, better control and higher yield. That makes metrology structurally more important.

Onto is less pure than some other names, but its breadth makes the stock more resilient. It is a quality name within the wider advanced packaging ecosystem.

Kulicke & Soffa $KLIC

Kulicke & Soffa is a smaller assembly equipment company. It has exposure to bonding, thermocompression bonding and other processes that become more important as chip architectures become more complex.

The upside can be above average if advanced packaging capex accelerates. KLIC is cyclical, but that also means the stock can react strongly when orders improve and investors revalue the backend of the semiconductor chain.

The risk is that the order cycle remains uneven. Still, KLIC fits the theme well. It is not at the front of the AI story, but it supplies technology needed to enable the next phase of packaging.

Veeco $VECO

Veeco is a smaller US equipment company with exposure to advanced packaging lithography. It is not a pure CoWoS play, but it is relevant for capacity expansions at IDMs and OSATs.

The upside lies in the possibility that investors look deeper into the AI supply chain. Veeco gets less attention than the large semiconductor equipment names, but specialized tools remain necessary as the backend becomes more complex.

The case is more indirect than Amkor or Camtek, but that also means the stock can surprise if the market broadens the theme. Within a strong capex cycle, Veeco can offer clear equipment leverage.

ASE Technology $ASX

ASE is one of the most important companies in the world in outsourced semiconductor assembly and test. If TSMC lacks sufficient CoWoS capacity, it is logical that ASE receives more attention from customers looking for additional advanced packaging capacity.

The upside is fundamentally strong because of scale, technical expertise and direct packaging exposure. ASE is better known than smaller niche companies, so the chance of an extreme re-rating may be lower. Its strategic relevance remains very high.

ASE is mainly a core name to follow the strength of the advanced packaging cycle. If demand continues to rise here, it confirms the broader investment case.

Powertech Technology

Powertech Technology is relevant because it is directly mentioned as a potential receiver of overflow orders. The company operates in assembly and test and has direct exposure to backend capacity.

The upside can be strong if investors start to believe these orders are part of a structural shift. Powertech is less familiar to Western investors, but operationally it sits close to the core of the problem.

Practical access to the stock may be more limited for European and US investors. Thematically, Powertech clearly belongs in this article. The company operates exactly in the layer where AI capacity is now becoming tight.

Conclusion

The AI cycle is broadening. GPUs remain important, but the next bottleneck is increasingly visible in advanced packaging, CoWoS capacity, substrates, bonding, testing and metrology. That is exactly the theme we have been highlighting for some time.

The reports around TSMC, ASE and Powertech make the signals stronger. The market is starting to see more clearly that AI is not only about the chip itself, but also about the infrastructure required to produce that chip at scale and make it work reliably.

We prefer companies with direct exposure to higher packaging capex and rising complexity. Amkor, AT&S, SÜSS MicroTec, Besi and Camtek stand out most clearly. ASE and Powertech remain important core names in the direct packaging chain, while FormFactor, Onto Innovation, Kulicke & Soffa and Veeco are interesting second-layer players.

We remain positive on this theme. The signals are becoming stronger and the market appears to be slowly confirming what we have thought for some time: the real AI leverage in the next phase may sit with the companies that make the chip chain scalable.

Disclaimer Aan de door ons opgestelde informatie kan op geen enkele wijze rechten worden ontleend. Alle door ons verstrekte informatie en analyses zijn geheel vrijblijvend. Alle consequenties van het op welke wijze dan ook toepassen van de informatie blijven volledig voor uw eigen rekening.

Wij aanvaarden geen aansprakelijkheid voor de mogelijke gevolgen of schade die zouden kunnen voortvloeien uit het gebruik van de door ons gepubliceerde informatie. U bent zelf eindverantwoordelijk voor de beslissingen die u neemt met betrekking tot uw beleggingen.