🧠 AI: Christopher Bloomstran ziet capex-cyclus als grote rekensom achter megacap tech

Volgens Christopher Bloomstran is AI geen lege hype. Hij erkent juist dat AI een technologie kan zijn die bedrijfsprocessen, software, productiviteit en infrastructuur blijvend verandert. Zijn waarschuwing gaat niet over de vraag of AI nuttig is. Zijn punt is dat de huidige investeringsgolf bij hyperscalers zo groot wordt dat de financiële rekensom steeds zwaarder weegt dan het groeiverhaal.

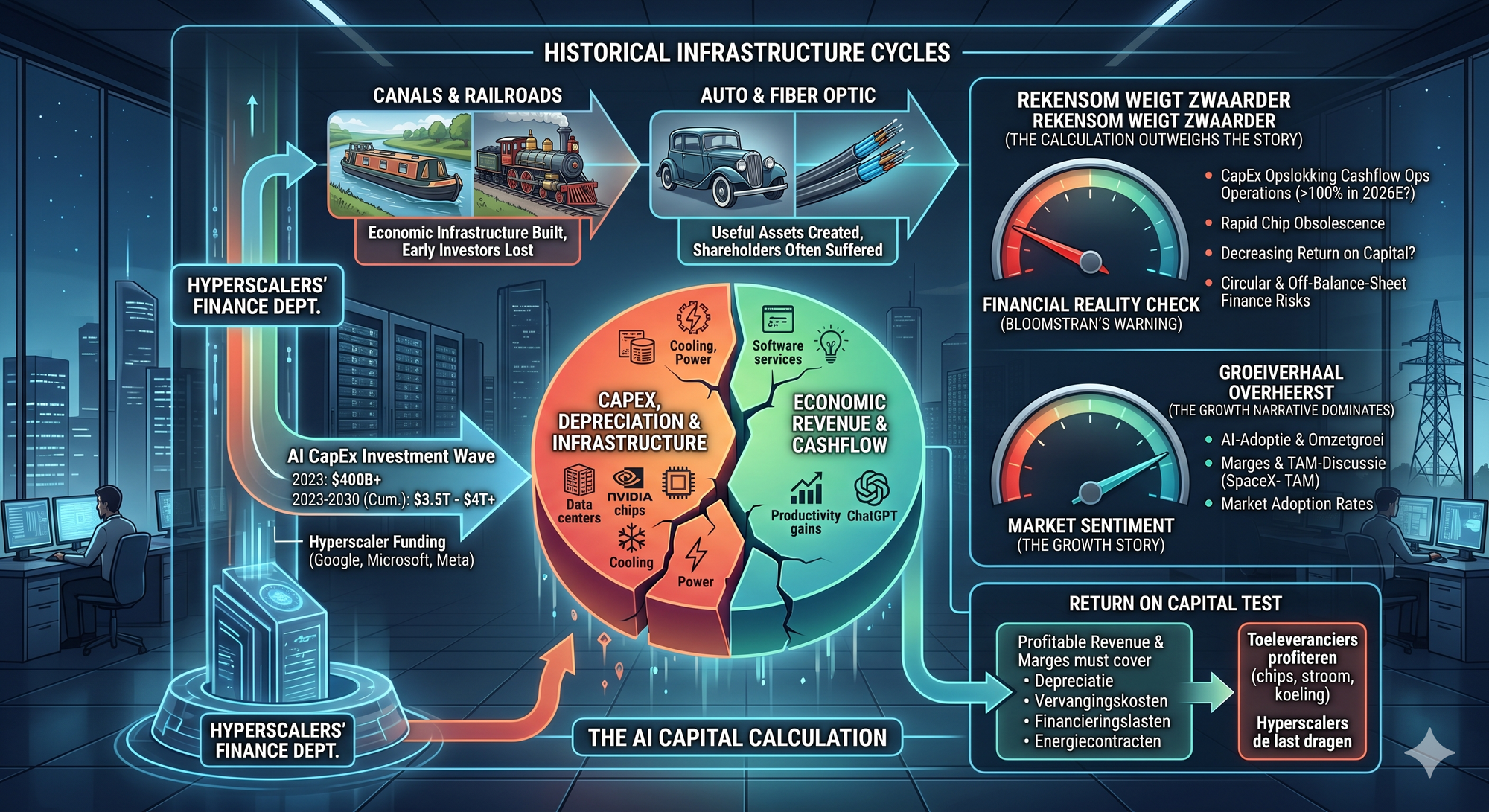

■ Volgens Bloomstran lijkt de huidige AI-golf op eerdere kapitaalcycli waarin de economie later profiteerde, maar veel investeerders onderweg geld verloren.

■ Hij ziet AI als een sterke technologie, maar niet automatisch als een sterke beleggingscase voor de hyperscalers die de infrastructuur financieren.

■ De kern van zijn analyse draait om CapEx, afschrijvingen, cashflowverbruik, off-balance-sheet financiering, circular finance en return on capital.

■ De bedragen zijn volgens hem inmiddels zo groot dat de markt niet meer alleen naar omzetgroei en adoptie kan kijken.

■ De centrale vraag is of Microsoft, Google, Meta en andere hyperscalers hun biljoeneninvesteringen ooit kunnen terugverdienen tegen aantrekkelijke rendementen.

Bloomstran plaatst de AI-CapEx-cyclus naast eerdere infrastructuurbooms, zoals kanalen, spoorwegen, auto’s en fiber. Die cycli leverden uiteindelijk vaak waardevolle infrastructuur op voor de economie. Voor veel eerste kapitaalverschaffers pakte het anders uit. De investeringen waren te vroeg, te groot of te duur. De infrastructuur bleef bestaan, maar de aandeelhouders kregen niet altijd het rendement waarvoor zij betaalden.

Investment view

De visie van Christopher Bloomstran is dat de AI-beleggingscase niet mag worden verward met de AI-technologie zelf. AI kan sterk zijn, breed worden toegepast en de economie productiever maken. Toch kan de kapitaalcyclus achter AI voor aandeelhouders minder aantrekkelijk uitpakken wanneer de investeringen te hoog worden en de returns dalen.

Jarenlang werden de grote technologiebedrijven gewaardeerd als kapitaallichte compounders. Zij hadden hoge marges, sterke vrije kasstromen, weinig balansdruk en returns op kapitaal in de lage tot midden 20%. Door AI verandert dat profiel. De hyperscalers moeten steeds meer investeren in datacenters, NVIDIA-chips, energie, koeling, netwerkcapaciteit en fysieke infrastructuur.

Volgens Bloomstran wordt daarmee de oude megacap-techcase minder schoon. De markt kijkt nog vaak naar AI als groeimotor, maar hij legt de nadruk op de economische opbrengst per geïnvesteerde dollar. Hoe hoger de CapEx, hoe hoger de toekomstige omzet en marge moeten zijn om dezelfde kwaliteit van rendement te behouden.

Zijn waarschuwing is daarom scherp. AI hoeft niet te mislukken om toch een probleem te worden voor beleggers. Het is genoeg als de technologie werkt, maar de kosten van de infrastructuur sneller stijgen dan de economische opbrengst.

De fibervergelijking

Bloomstran gebruikt fiber als historisch ankerpunt. Tijdens de telecom- en internetboom werd enorme glasvezelinfrastructuur aangelegd. Die infrastructuur bleek later essentieel voor het internet zoals we dat nu kennen. Zonder fiber waren diensten zoals YouTube, Netflix en grootschalige cloudtoepassingen moeilijker op deze schaal ontstaan.

Voor de eerste investeerders was het verhaal minder gunstig. Volgens Bloomstran bedroeg de fiber-boom destijds ongeveer 1% van het BBP. In 2021 zou slechts ongeveer 4% van de aangelegde fiber daadwerkelijk zijn gebruikt. Daarmee wil hij laten zien dat nuttige infrastructuur ook veel te vroeg of veel te agressief kan worden gebouwd.

Die vergelijking gebruikt hij nu voor AI. Datacenters, chips en netwerken kunnen later onmisbaar blijken. De vraag blijft of de bedrijven die vandaag de grootste cheques uitschrijven, daar voldoende rendement op behalen. Economische waarde voor de samenleving en aandeelhoudersrendement vallen niet automatisch samen.

De schaal van de AI-CapEx

Volgens Bloomstran lag de hyperscaler-CapEx vorig jaar rond 400 miljard dollar. In eerdere analyses werd al gesproken over ongeveer 750 miljard dollar. Door nieuwe aankondigingen van onder meer Google ligt het eindpunt mogelijk veel hoger.

Hij noemt inmiddels ongeveer 1,3 tot 1,4 biljoen dollar aan CapEx die al is uitgegeven of vastgelegd. Voor de periode 2023 tot 2030 noemt hij cumulatieve bedragen van 3,5 tot 4 biljoen dollar. Hogere ramingen gaan richting 7 biljoen dollar.

Die bedragen zetten de hele AI-discussie op scherp. Bij 400 miljard dollar CapEx en een afschrijving over tien jaar ontstaat jaarlijks 40 miljard dollar aan depreciation. Wanneer op diezelfde 400 miljard dollar een return van 15% nodig is, vraagt dat om ongeveer 60 miljard dollar aan extra opbrengst. Dat is de rekensom voor één jaar aan investeringen.

Bij 4 biljoen dollar cumulatieve CapEx wordt de lat veel hoger. Wanneer 10% daarvan jaarlijks als omzet moet terugkomen, gaat het om 400 miljard dollar per jaar. Bij een gewenste return van 20% op 4 biljoen dollar is ongeveer 800 miljard dollar economische opbrengst nodig. Dat is zelfs voor megacap tech een zware opgave.

De omzet moet de investeringen nog bewijzen

Bloomstran plaatst de AI-omzet naast de omvang van de investeringen. Hij noemt Anthropic met een run-rate van ongeveer 47 miljard dollar en ChatGPT met ongeveer 25 miljard dollar. Dat zijn stevige bedragen, maar ze staan nog niet in verhouding tot de infrastructuur die nu wordt gebouwd.

Ook kijkt hij naar de bestaande schaal van de hyperscalers. Microsoft zou rond 300 miljard dollar omzet zitten. Google zou rond 400 miljard dollar omzet zitten. De cashflow from operations van deze bedrijven ligt volgens hem rond 150 miljard dollar per jaar.

Daarmee wordt de druk zichtbaar. Als de investeringen blijven oplopen, moet AI niet alleen extra omzet genereren. Die omzet moet groot genoeg zijn om afschrijvingen, vervangingskosten, financieringslasten, energiecontracten en gewenste returns te dragen.

Bloomstran plaatst dat tegen de bredere markt. De boekwaarde van de S&P 500 ligt volgens hem rond 10,5 biljoen dollar. De totale omzet van de index ligt rond 20 biljoen dollar. Tegen die achtergrond is een AI-CapEx-cyclus van 4, 5, 6 of 7 biljoen dollar uitzonderlijk groot.

Afschrijvingen veranderen de winstkwaliteit

Depreciation is volgens Bloomstran een van de onderschatte risico’s. Zolang datacenters worden gebouwd en chips worden gekocht, kijkt de markt vooral naar groei. Daarna komen de afschrijvingen door de resultatenrekening heen.

Dat maakt de discussie over de levensduur van NVIDIA-chips en datacenters relevant. Hyperscalers kunnen afschrijvingstermijnen verlengen van drie tot vier jaar naar vijf tot zes jaar. Boekhoudkundig ondersteunt dat de winst. Economisch blijft de vraag hoe snel deze infrastructuur moet worden vervangen.

AI-chips verouderen snel. Modellen vragen steeds meer rekenkracht. Datacenters hebben meer stroom, koeling en netwerkcapaciteit nodig. Een langere afschrijvingstermijn verandert niets aan de fysieke noodzaak om te blijven investeren.

Voor Bloomstran draait het daarom om vrije kasstroom na onderhoud, vervanging en uitbreiding. Omzetgroei is pas waardevol wanneer zij overblijft als cashflow met voldoende rendement op het kapitaal dat ervoor nodig was.

CapEx slokt de kasstroom op

Bloomstran noemt concrete percentages voor de grote geïntegreerde technologiebedrijven. In 2023 bedroeg CapEx ongeveer 11,9% van de omzet. Afgerond is dat 12%. Die CapEx verbruikte toen ongeveer 41% van cash from operations.

Volgens zijn analyse loopt dat snel op. Richting 2026 kan CapEx 100% van cash from operations opslokken. Hij suggereert zelfs dat het boven 100% kan uitkomen.

Dat is een grote breuk met het oude beeld van megacap tech. Deze bedrijven stonden bekend om enorme vrije kasstromen, hoge marges en grote aandeleninkoopprogramma’s. Wanneer CapEx bijna alle operationele kasstroom gebruikt, verandert de kapitaalallocatie. Buybacks dalen. Leverage loopt op. De multiple hoort dan kritischer te worden.

De markt betaalt graag voor groei met hoge vrije kasstroom. Een bedrijf dat steeds meer moet investeren om zijn positie te verdedigen, verdient een andere beoordeling.

Return on capital wordt de echte test

Volgens Bloomstran draait de hele AI-rekensom uiteindelijk om return on capital. Microsoft, Google, Meta en andere grote technologiebedrijven konden jarenlang hoge returns behalen omdat hun modellen relatief kapitaallicht waren. AI duwt hen richting een infrastructuurprofiel.

Op 4 biljoen dollar CapEx vraagt een return van 20% om ongeveer 800 miljard dollar economische opbrengst. Dat moet niet alleen omzet zijn. Het moet winstgevende omzet zijn, met voldoende marge en cashflow.

Daar komt concurrentie bij. Meerdere hyperscalers bouwen tegelijk capaciteit. Als zes of zeven aanbieders dezelfde markt bedienen, krijgen klanten onderhandelingsmacht. Prijzen kunnen dalen. Capaciteit kan dubbel worden gebouwd. Marges kunnen onder druk komen.

Volgens Bloomstran is dat het klassieke patroon in kapitaalintensieve sectoren. Eerst bouwen bedrijven agressief, daarna komt prijsdruk, vervolgens zakt het rendement op kapitaal. De technologie kan nuttig blijven, terwijl de beurscase verslechtert.

Off-balance-sheet financiering vergroot het risico

Bloomstran wijst op ongeveer 650 miljard dollar aan off-balance-sheet financiering. Daarmee bedoelt hij financiering die niet volledig zichtbaar is als traditionele schuld op de balans van de hyperscalers. Het gaat om joint ventures, special purpose vehicles, private capital, verzekeraars en leaseachtige structuren.

Het voorbeeld van Meta en Hyperion in Louisiana is volgens hem illustratief. Hij noemt een datacenterproject van ongeveer 30 miljard dollar. Meta zou 20% van de equitylaag inbrengen, volgens Bloomstran ongeveer 500 miljoen dollar binnen die structuur. De rest wordt deels via partijen als Blue Owl gefinancierd.

De economische verplichting verdwijnt daarmee niet. Als Meta garanties geeft of contractueel verbonden blijft met het project, blijft het risico bestaan. Het staat alleen anders verpakt.

Bloomstran waarschuwt daarom dat beleggers niet alleen naar gerapporteerde schuld moeten kijken. De echte vraag is welke verplichtingen, garanties, leases en afnamecontracten economisch bij de hyperscaler horen.

Private capital wordt onderdeel van de AI-keten

De AI-infrastructuur wordt steeds vaker gefinancierd via private capital en gespecialiseerde vehikels. Voor hyperscalers is dat aantrekkelijk, omdat grote datacenterprojecten kunnen worden gebouwd zonder dat de volledige kapitaallast direct als gewone balansschuld verschijnt.

Voor beleggers maakt dit de analyse lastiger. De gerapporteerde balans kan beheersbaar ogen, terwijl de economische exposure groter is. Dat geldt vooral bij projecten met lange looptijden, hoge energievraag en snelle technologische veroudering.

Bloomstran ziet hierin een duidelijk patroon. Wanneer een kapitaalcyclus complexere financiering nodig heeft om door te groeien, moet de markt scherper kijken naar kwaliteit van cashflow en balansrisico.

Circular finance binnen het AI-ecosysteem

Bloomstran wijst ook op circular finance. Daarmee bedoelt hij kapitaalstromen waarbij leveranciers, klanten en partners elkaar financieren, waarna dezelfde partijen weer elkaars producten of capaciteit kopen.

Een voorbeeld is NVIDIA. Wanneer NVIDIA investeert in klanten of partners die daarna NVIDIA-chips kopen, ontstaat een geldstroom binnen dezelfde keten. Dat betekent niet automatisch dat de vraag kunstmatig is. Het maakt de kwaliteit van de omzet wel belangrijker.

Ook situaties waarin chips als onderpand worden gebruikt passen in dit beeld. Hardware wordt dan niet alleen operationeel bezit, maar ook financieringsbasis.

De vraag wordt daardoor scherper: hoeveel omzet komt uit echte externe eindvraag en hoeveel wordt versterkt door investeringen, garanties en financiering binnen het AI-ecosysteem zelf? Voor Bloomstran is dat een rood vlag-signaal in de analyse van deze cyclus.

De S&P 500 wordt gevoeliger voor AI-CapEx

De grote AI-hyperscalers hebben een zware weging in de S&P 500. Daardoor wordt de index gevoeliger voor veranderingen in hun winstkwaliteit, kapitaalintensiteit en returns.

Bloomstran plaatst dat naast de boekwaarde van de S&P 500 van ongeveer 10,5 biljoen dollar en totale omzet van ongeveer 20 biljoen dollar. Als een klein aantal megacaps meerdere biljoenen dollars aan AI-infrastructuur moet financieren, wordt dat niet langer een nicheprobleem. Het raakt de waardering van de brede markt.

Dat betekent niet dat de rally direct eindigt. Bloomstran geeft juist aan dat de cyclus mogelijk nog langer kan doorlopen. De markt kan voorlopig blijven reageren op groei, chips, datacenters, power, koeling en AI-adoptie.

De onderliggende kwaliteit verandert wel. De oude megacap-techcase draaide om hoge marges en sterke vrije kasstroom. De nieuwe AI-case vraagt om voortdurende investeringen in fysieke assets. Dat verschil moet in de waardering worden meegenomen.

Leveranciers kunnen beter gepositioneerd zijn

Bloomstran ziet binnen de AI-cyclus niet alleen risico. Toeleveranciers kunnen juist profiteren zolang de investeringsgolf doorgaat. Denk aan chips, stroomoplossingen, koeling, datacenterbouw, netwerkcapaciteit en optische verbindingen.

Hij noemt Cummins als voorbeeld. Het bedrijf profiteert van de vraag naar back-up power en front-scale power voor datacenters. Daarmee raakt hij een breder punt: de bottleneck ligt niet alleen bij GPU’s. Energie, koeling en fysieke beschikbaarheid van infrastructuur worden steeds bepalender.

Voor beleggers maakt dat de AI-trade selectiever. De hyperscalers dragen de kapitaallast. Sommige leveranciers kunnen juist earnings leverage krijgen door de bouwgolf zelf.

SpaceX en de TAM-discussie

Bloomstran haalt ook SpaceX aan om te laten zien hoe groot sommige marktverhalen worden gemaakt. Hij verwijst naar een TAM van 28,5 biljoen dollar. TAM staat voor Total Addressable Market. Dat is de totale markt die een bedrijf theoretisch zou kunnen bedienen als alles maximaal meezit.

Ter vergelijking noemt hij een wereldwijde economie van ongeveer 120 biljoen dollar en een Amerikaanse economie van ongeveer 32 biljoen dollar. Daarmee zet hij de SpaceX-TAM bewust in perspectief.

Zijn punt is dat beleggers kritisch moeten blijven wanneer een marktverhaal bijna de omvang krijgt van de volledige Amerikaanse economie. Een grote markt kan bestaan, maar een extreem hoge TAM wordt vaak gebruikt om een hoge waardering te onderbouwen. Voor Bloomstran past dat bij kapitaalcycli waarin het verhaal steeds groter wordt naarmate er meer geld nodig is.

Wat beleggers moeten meenemen

De analyse van Christopher Bloomstran dwingt beleggers om AI niet alleen als groeiverhaal te behandelen. De technologie kan sterk zijn, de adoptie kan doorgaan en de infrastructuur kan later onmisbaar blijken. Toch blijft de financiële uitkomst onzeker zolang de CapEx sneller groeit dan bewezen economische opbrengst.

De belangrijkste meetpunten zijn CapEx als percentage van omzet, CapEx als percentage van cashflow, afschrijvingen, vervangingskosten, off-balance-sheet verplichtingen, circular finance en return on capital.

De grootste fout is technologische kracht automatisch vertalen naar aandeelhoudersrendement. Bloomstran laat zien dat die stap niet vanzelfsprekend is.

Conclusie

Volgens Christopher Bloomstran is AI waarschijnlijk een grote technologische doorbraak, maar de kapitaalcyclus achter AI wordt steeds zwaarder. Zijn waarschuwing draait om de rekensom. De investeringen zijn inmiddels zo groot dat omzet, marges en cashflows uitzonderlijk hard moeten groeien om de huidige waarderingen te rechtvaardigen.

De cijfers maken zijn analyse stevig. Fiber vertegenwoordigde destijds ongeveer 1% van het BBP, terwijl in 2021 slechts ongeveer 4% van de aangelegde capaciteit zou zijn gebruikt. De huidige AI-CapEx ligt al op honderden miljarden dollars per jaar, met cumulatieve ramingen van 3,5 tot 4 biljoen dollar en scenario’s richting 7 biljoen dollar. Bij zulke bedragen worden afschrijvingen, cashflowverbruik en return on capital bepalend.

Voor beleggers is de les helder. AI kan de wereld veranderen, maar dat garandeert niet dat hyperscalers hun biljoeneninvesteringen tegen aantrekkelijke rendementen terugverdienen. De markt moet minder leunen op het verhaal en harder kijken naar de rekensom. Dat is de kern van Bloomstrans waarschuwing.

English version

Christopher Bloomstran sees the AI CapEx cycle as the key calculation behind megacap tech

Introduction

According to Christopher Bloomstran, AI is not an empty hype. He acknowledges that AI can become a technology that permanently changes business processes, software, productivity and infrastructure. His warning is not about whether AI is useful. His point is that the current investment wave among hyperscalers has become so large that the financial calculation increasingly matters more than the growth narrative.

Bloomstran compares the AI CapEx cycle with earlier infrastructure booms, including canals, railroads, automobiles and fiber. Those cycles often created valuable infrastructure for the economy. For the first capital providers, the outcome was frequently different. The investments were too early, too large or too expensive. The infrastructure survived, but shareholders did not always earn the return they expected.

■ According to Bloomstran, the current AI wave resembles earlier capital cycles where the economy later benefited, while many investors lost money along the way.

■ He sees AI as a strong technology, but not automatically as a strong investment case for the hyperscalers financing the infrastructure.

■ His analysis focuses on CapEx, depreciation, cash flow absorption, off-balance-sheet financing, circular finance and return on capital.

■ The numbers have become so large that the market can no longer look only at revenue growth and adoption.

■ The central question is whether Microsoft, Google, Meta and other hyperscalers can ever earn attractive returns on trillions of dollars of investment.

Investment view

Christopher Bloomstran’s view is that the AI investment case should not be confused with the AI technology itself. AI can be powerful, widely adopted and productivity enhancing. Yet the capital cycle behind AI can still become less attractive for shareholders if the investments become too large and returns decline.

For years, the major technology companies were valued as capital-light compounders. They had high margins, strong free cash flow, limited balance sheet pressure and returns on capital in the low to mid-20% range. AI changes that profile. The hyperscalers must invest more heavily in data centers, NVIDIA chips, power, cooling, network capacity and physical infrastructure.

That makes the old megacap tech case less clean. The market still often sees AI as a growth engine, while Bloomstran focuses on the economic output per invested dollar. The higher the CapEx, the more future revenue and margin are required to preserve the same quality of return.

His warning is sharp. AI does not have to fail to become a problem for investors. It is enough for the technology to work while the cost of the infrastructure rises faster than the economic payoff.

The fiber comparison

Bloomstran uses fiber as a historical anchor. During the telecom and internet boom, enormous fiber infrastructure was built. That infrastructure later became essential for the internet as we know it today. Without fiber, services such as YouTube, Netflix and large-scale cloud applications would have been harder to build at their current scale.

For the first investors, the story was less favorable. According to Bloomstran, the fiber boom represented about 1% of GDP at the time. By 2021, only about 4% of the installed fiber capacity had reportedly been used. His point is that useful infrastructure can be built far too early or far too aggressively.

He now applies that comparison to AI. Data centers, chips and networks may later prove indispensable. The question is whether the companies writing the largest checks today will earn sufficient returns. Economic value for society and shareholder returns do not automatically move together.

The scale of AI CapEx

According to Bloomstran, hyperscaler CapEx was around $400 billion last year. Earlier analyses already discussed roughly $750 billion. New announcements from companies such as Google suggest the endpoint could be much higher.

He now refers to roughly $1.3 trillion to $1.4 trillion of CapEx already spent or committed. For the 2023 to 2030 period, he mentions cumulative figures of $3.5 trillion to $4 trillion. Higher estimates move toward $7 trillion.

Those numbers change the entire AI debate. At $400 billion of CapEx depreciated over ten years, annual depreciation reaches $40 billion. If that same $400 billion requires a 15% return, it needs roughly $60 billion of additional economic output. That is the calculation for only one year of investment.

At $4 trillion of cumulative CapEx, the hurdle becomes far higher. If 10% of that amount must return annually as revenue, the figure is $400 billion per year. If a 20% return is required on $4 trillion, roughly $800 billion of economic output is needed. Even for megacap tech, that is a demanding hurdle.

Revenue still has to prove the investment case

Bloomstran places AI revenue next to the scale of the investments. He mentions Anthropic at a run rate of roughly $47 billion and ChatGPT at about $25 billion. Those are strong figures, but they remain small compared with the infrastructure now being built.

He also looks at the existing scale of the hyperscalers. Microsoft is around $300 billion in revenue. Google is around $400 billion. Cash flow from operations at these companies is roughly $150 billion per year, according to his analysis.

That shows the pressure. If investments keep rising, AI must do more than generate extra revenue. That revenue must be large enough to carry depreciation, replacement costs, financing costs, power contracts and required returns.

Bloomstran also compares this with the broader market. The book value of the S&P 500 is around $10.5 trillion. Total revenue for the index is around $20 trillion. Against that backdrop, an AI CapEx cycle of $4 trillion, $5 trillion, $6 trillion or $7 trillion is exceptionally large.

Depreciation changes earnings quality

Depreciation is one of the underappreciated risks in Bloomstran’s analysis. While data centers are being built and chips are being purchased, the market mostly looks at growth. After that, depreciation flows through the income statement.

That makes the debate about the useful life of NVIDIA chips and data centers relevant. Hyperscalers can extend depreciation schedules from three to four years to five to six years. From an accounting perspective, that supports earnings. Economically, the question remains how quickly the infrastructure must be replaced.

AI chips age quickly. Models require more compute. Data centers need more power, cooling and network capacity. A longer depreciation schedule does not change the physical need to keep investing.

For Bloomstran, the issue is free cash flow after maintenance, replacement and expansion. Revenue growth is only valuable when it translates into cash flow with sufficient return on the capital required to generate it.

CapEx absorbs the cash flow

Bloomstran cites specific percentages for the large integrated technology companies. In 2023, CapEx was about 11.9% of revenue. Rounded, that is 12%. That CapEx consumed about 41% of cash flow from operations.

According to his analysis, this rises quickly. By 2026, CapEx could absorb 100% of cash flow from operations. He even suggests it could exceed 100%.

That is a major break from the old megacap tech profile. These companies were known for enormous free cash flow, high margins and large share repurchase programs. When CapEx consumes nearly all operating cash flow, capital allocation changes. Buybacks decline. Leverage rises. The multiple deserves more scrutiny.

The market likes growth with high free cash flow. A company that must invest more and more simply to defend its position deserves a different assessment.

Return on capital becomes the real test

According to Bloomstran, the entire AI calculation ultimately comes down to return on capital. Microsoft, Google, Meta and other major technology companies were able to generate high returns for years because their models were relatively capital-light. AI pushes them toward an infrastructure profile.

On $4 trillion of CapEx, a 20% return requires roughly $800 billion of economic output. That cannot just be revenue. It must be profitable revenue, with sufficient margin and cash flow.

Competition adds another layer. Multiple hyperscalers are building capacity at the same time. If six or seven providers serve the same market, customers gain bargaining power. Prices can fall. Capacity can be duplicated. Margins can come under pressure.

Bloomstran sees this as the classic pattern in capital-intensive industries. Companies build aggressively first, pricing pressure follows, then return on capital declines. The technology can remain useful while the equity case deteriorates.

Off-balance-sheet financing increases the risk

Bloomstran points to roughly $650 billion of off-balance-sheet financing. By that, he means financing that is not fully visible as traditional debt on the hyperscalers’ balance sheets. This includes joint ventures, special purpose vehicles, private capital, insurers and lease-like structures.

The example of Meta and Hyperion in Louisiana is illustrative. He refers to a data center project of roughly $30 billion. Meta would contribute 20% of the equity layer, according to Bloomstran roughly $500 million within that structure. The rest is partly financed through parties such as Blue Owl.

The economic obligation does not disappear. If Meta provides guarantees or remains contractually tied to the project, the risk remains. It is simply packaged differently.

Bloomstran therefore warns that investors should not look only at reported debt. The real question is which obligations, guarantees, leases and offtake agreements economically belong to the hyperscaler.

Private capital becomes part of the AI chain

AI infrastructure is increasingly financed through private capital and specialized vehicles. For hyperscalers, this is attractive because large data center projects can be built without the full capital burden appearing immediately as ordinary balance sheet debt.

For investors, this makes the analysis harder. The reported balance sheet can look manageable while the economic exposure is larger. This is especially relevant for projects with long durations, high power demand and rapid technological aging.

Bloomstran sees a clear pattern here. When a capital cycle requires more complex financing to keep growing, the market must pay closer attention to cash flow quality and balance sheet risk.

Circular finance within the AI ecosystem

Bloomstran also points to circular finance. This refers to capital flows where suppliers, customers and partners finance one another, after which the same parties buy each other’s products or capacity.

One example is NVIDIA. If NVIDIA invests in customers or partners that later buy NVIDIA chips, money moves inside the same chain. That does not automatically make the demand artificial. It does make the quality of revenue more important.

Situations where chips are used as collateral fit the same pattern. Hardware then becomes not only an operating asset, but also a financing base.

The question becomes sharper: how much revenue comes from real external end demand, and how much is amplified by investments, guarantees and financing inside the AI ecosystem itself? For Bloomstran, that is a red-flag signal in the analysis of this cycle.

The S&P 500 becomes more sensitive to AI CapEx

The major AI hyperscalers carry heavy weight in the S&P 500. That makes the index more sensitive to changes in their earnings quality, capital intensity and returns.

Bloomstran places this next to the S&P 500 book value of roughly $10.5 trillion and total revenue of about $20 trillion. If a small number of megacaps must finance several trillions of dollars of AI infrastructure, this is no longer a niche issue. It affects broad market valuation.

That does not mean the rally has to end immediately. Bloomstran suggests the cycle could continue longer than many skeptics expect. The market can keep responding to growth, chips, data centers, power, cooling and AI adoption for now.

The underlying quality still changes. The old megacap tech case was built on high margins and strong free cash flow. The new AI case requires continuous investment in physical assets. That difference should be reflected in valuation.

Suppliers may be better positioned

Bloomstran does not see only risk inside the AI cycle. Suppliers can benefit as long as the investment wave continues. This includes chips, power solutions, cooling, data center construction, network capacity and optical connections.

He mentions Cummins as an example. The company benefits from demand for backup power and front-scale power for data centers. This speaks to a broader issue: the bottleneck is not only GPUs. Power, cooling and physical infrastructure availability are becoming increasingly decisive.

For investors, that makes the AI trade more selective. Hyperscalers carry the capital burden. Some suppliers can gain earnings leverage from the construction cycle itself.

SpaceX and the TAM debate

Bloomstran also refers to SpaceX to show how large some market narratives can become. He points to a TAM of $28.5 trillion. TAM stands for Total Addressable Market. It means the total market a company could theoretically serve if everything goes right.

For comparison, he mentions a global economy of roughly $120 trillion and a U.S. economy of roughly $32 trillion. He uses this comparison to put the SpaceX TAM into perspective.

His point is that investors should remain critical when a market story almost reaches the size of the entire U.S. economy. A large market can exist, but an extremely high TAM is often used to support a high valuation. For Bloomstran, this fits capital cycles where the story grows larger as more money is required.

What investors should take away

Christopher Bloomstran’s analysis forces investors to treat AI as more than a growth story. The technology can be strong, adoption can continue and the infrastructure may later prove indispensable. The financial outcome remains uncertain as long as CapEx grows faster than proven economic output.

The key metrics are CapEx as a percentage of revenue, CapEx as a percentage of cash flow, depreciation, replacement costs, off-balance-sheet obligations, circular finance and return on capital.

The biggest mistake is to automatically translate technological strength into shareholder return. Bloomstran shows why that step is not automatic.

Conclusion

According to Christopher Bloomstran, AI is probably a major technological breakthrough, but the capital cycle behind AI is becoming heavier. His warning is about the calculation. The investments have become so large that revenue, margins and cash flows must grow exceptionally fast to justify current valuations.

The numbers make his analysis forceful. Fiber represented about 1% of GDP at the time, while only about 4% of installed capacity was reportedly used by 2021. Current AI CapEx is already running at hundreds of billions of dollars per year, with cumulative estimates of $3.5 trillion to $4 trillion and scenarios moving toward $7 trillion. At those levels, depreciation, cash flow absorption and return on capital become decisive.

For investors, the lesson is clear. AI can change the world, but that does not guarantee that hyperscalers will earn attractive returns on trillions of dollars of investment. The market should rely less on the story and look harder at the calculation. That is the core of Bloomstran’s warning.

Disclaimer Aan de door ons opgestelde informatie kan op geen enkele wijze rechten worden ontleend. Alle door ons verstrekte informatie en analyses zijn geheel vrijblijvend. Alle consequenties van het op welke wijze dan ook toepassen van de informatie blijven volledig voor uw eigen rekening.

Wij aanvaarden geen aansprakelijkheid voor de mogelijke gevolgen of schade die zouden kunnen voortvloeien uit het gebruik van de door ons gepubliceerde informatie. U bent zelf eindverantwoordelijk voor de beslissingen die u neemt met betrekking tot uw beleggingen.