🍀 DipRip: Buy the Dip & Sell the Rip: Weer aandeel in memory op Wall Street kopen

For our international clients: English version is provided after the Dutch text

Heb je vragen en heb je een jaarabonnement bij ons, dan kan je altijd via info@scetrader.nl een mail sturen. Ook kan je een verzoek indienen zodat we telefonisch even contact met elkaar hebben als je meer uitleg wilt.

Wil je alle artikelen kunnen lezen en elke podcast beluisteren? Neem dan een abonnement en krijg toegang tot alle artikelen en de database met duizenden berichten.

We gaan een actie, een aanpassing, uitvoeren binnen het onderdeel buy the dip and sell the rip.

Alle berichten van dit onderdeel zijn te vinden door te zoeken op 'diprip'. Dit zijn speculatieve of trading posities die overigens vaak ook langer worden aangehouden.

Let op: deze porfolio staat los van alle andere portfolio's en berichtgeving en kan dus ingaan tegen onze langere visie of ideeën.

Het aandeel

Axcelis Technologies $ACLS is een toonaangevende leverancier van ion-implantatie-apparatuur voor de halfgeleiderindustrie. Het bedrijf levert systemen die cruciaal zijn voor de productie van chips, waaronder mature nodes, silicon carbide (SiC) en geheugenchips zoals DRAM, NAND en high-bandwidth memory (HBM).

Wij gaan kopen. Axcelis biedt beleggers een unieke kans om in te spelen op de explosieve groei van de halfgeleidersector, met een bijzondere nadruk op de memory-markt.

Hoewel het bedrijf in de zomermaanden van 2025 te maken had met een tijdelijke dip als gevolg van de cyclische vertraging in mature nodes en geheugenchips, ligt de focus nu duidelijk op de veelbelovende fase die vanaf 2026 wordt verwacht.

De structurele vraag naar kunstmatige intelligentie, datacenters en elektrische voertuigen zal de motor zijn van dit herstel, en Axcelis bevindt zich in een uitstekende positie om hiervan te profiteren.

Waardering en orderbacklog

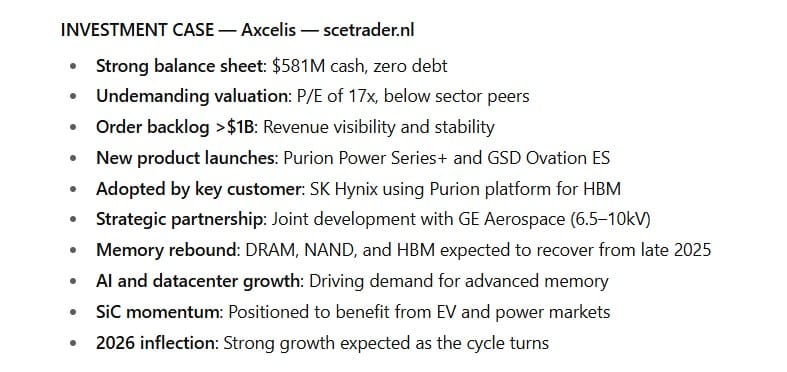

De waardering van het aandeel bevestigt dat er sprake is van een aantrekkelijke instapkans. Met een koers-winstverhouding van 17 keer noteert Axcelis duidelijk onder het gemiddelde van sectorgenoten, wat wijst op onderwaardering ten opzichte van de brede halfgeleiderindustrie.

Daarbij komt dat het bedrijf over een orderbacklog van meer dan $1 miljard beschikt, waardoor de omzet voor de komende kwartalen al voor een belangrijk deel is afgedekt.

Dit biedt beleggers niet alleen zichtbaarheid en stabiliteit, maar ook de geruststelling dat er een solide basis ligt om toekomstige groei op te bouwen.

Purion Power Series+

Een andere doorslaggevende factor is de introductie van de Purion Power Series+, die op 9 september 2025 werd gelanceerd. Dit nieuwe platform is specifiek ontworpen voor de productie van next-gen memory en power devices en bevestigt de rol van Axcelis als toonaangevende leverancier in een markt die steeds complexer en kapitaalintensiever wordt.

SK Hynix

Het bedrijf heeft bovendien bewezen klanten aan zich te binden die wereldwijd leidend zijn in memory-productie. Een voorbeeld hiervan is SK Hynix, dat een centrale rol speelt in de ontwikkeling van high-bandwidth memory (HBM). De keuze van dit soort klanten voor de technologie van Axcelis toont het strategische belang van het Purion-platform en verstevigt het groeipotentieel van het bedrijf.

Dat alles bij elkaar

Met een uitzonderlijk sterke balans, met $581 miljoen aan cash en geen schuldenlast zien we dit aandeel als een mooie kans (geen garanties). De balans geeft het bedrijf niet alleen de veerkracht om cyclische dippen te doorstaan, maar ook de flexibiliteit om te blijven investeren in R&D, nieuwe productintroducties en strategische samenwerkingen.

Alles bij elkaar maakt dit Axcelis tot een aandeel dat nu op een interessant kantelpunt staat. De huidige waardering is aantrekkelijk, de financiële fundamenten zijn ijzersterk en de vraag naar memory-chips staat op het punt van een krachtige heropleving.

Wij zien dit daarom als hét moment om in te stappen, door de memory-rebound die heel hard gaat. De stijging hoeft niet in een rechte lijn te zijn, maar als de huidige trend in memory doorzet, kan de rally wel eens heel fors zijn.

Memory-chips als katalysator

De kracht van Axcelis ligt in de directe blootstelling aan de snelgroeiende geheugenchipmarkt, die onmisbaar is voor toepassingen in kunstmatige intelligentie, datacenters en high-performance computing.

Terwijl de totale omzet momenteel nog grotendeels wordt gedragen door mature nodes en SiC, positioneert het bedrijf zich steeds sterker richting memory.

Tijdens de Q2 2025 earnings call (5 augustus 2025) gaf Axcelis aan dat memory-toepassingen slechts 3% van de systems-omzet vertegenwoordigden.

Dit lijkt beperkt, maar het management ziet dit als het begin van een significante groeicurve. Met name de vraag naar HBM (high-bandwidth memory), een cruciale component voor GPU’s die AI-workloads draaien, biedt enorme kansen.

De Purion-familie is hierbij doorslaggevend. Dit platform levert low-energy boron-implants die de productieopbrengsten (yields) van DRAM, NAND en HBM verbeteren. Axcelis benadrukte dat deze technologie inmiddels is opgenomen in productielijnen van vooraanstaande klanten, waaronder SK Hynix, dat wereldwijd een sleutelspeler is in HBM.

Op 9 september 2025 lanceerde Axcelis de Purion Power Series+, een nieuw systeem dat niet alleen superjunction-architecturen in power devices ondersteunt, maar ook wordt toegepast in memory-processen.

Daarmee positioneert Axcelis zich nog sterker in dit segment, precies op het moment dat de markt zich opmaakt voor een heropleving.

Volgens de Q2 2025 10-Q bevindt de memory-markt zich nu in een cyclische dip door overcapaciteit, maar het management herhaalde op 5 augustus dat vanaf eind 2025 een krachtig herstel wordt verwacht.

De drijvende krachten zijn de massale investeringen in datacenters en de explosieve groei van AI-applicaties. Axcelis voorziet daardoor in 2026 een forse toename van memory-gerelateerde orders, wat de omzetbasis structureel zal verbreden.

Laatste cijfers en outlook

Q2 2025 (gerapporteerd 5 augustus 2025):

- Omzet: $194,5 miljoen, -24,2% YoY (vs. $256,7 miljoen in Q2 2024).

- GAAP-brutomarge: 44,9% (non-GAAP: 45,2%).

- Operationele marge: 14,9% (non-GAAP: 17,7%).

- GAAP-diluted EPS: $0,98 (non-GAAP: $1,13).

- Cashpositie: $581 miljoen (geen schulden).

Guidance (Q3 2025, eindigend 30 september 2025):

- Omzet: ca. $200 miljoen.

- EPS: GAAP $0,87, non-GAAP $1,00.

Vooruitzichten (gegeven op 5 augustus 2025):

- Jaaromzet 2025: ca. $800 miljoen.

- Cyclische bodem in 2025, herstel in memory en SiC-markten verwacht in 2026.

Positieve catalysts

Axcelis heeft een reeks aan groeidrijvers die de komende kwartalen en jaren hun effect zullen laten zien. De lancering van de Purion Power Series+ en de GSD Ovation ES in september 2025 markeert Axcelis’ toegenomen innovatiekracht. Deze systemen zijn ontworpen om te voldoen aan de strengere eisen van next-gen chiparchitecturen, waardoor Axcelis optimaal kan profiteren van de groei in HBM en SiC.

Daarnaast werd in augustus 2025 een joint development program met GE Aerospace aangekondigd, gericht op toepassingen in elektrische voertuigen en vermogenselektronica (6.5-10kV). Samenwerkingen van dit type versterken de positionering van Axcelis in sectoren die nauw verbonden zijn met de energietransitie en de elektrificatie van transport.

De orderbacklog van meer dan $1 miljard, bevestigd op 5 augustus 2025, biedt een stabiele basis en duidelijke zichtbaarheid richting toekomstige omzet. Tegelijkertijd verstevigde Axcelis zijn internationale profiel met deelname aan SEMICON China (juni 2025), waar nieuwe oplossingen werden gepresenteerd aan belangrijke memory-klanten.

Het management benadrukte bovendien dat vanaf 2026 een sterke marktvraag naar zowel HBM als SiC wordt verwacht, gedreven door AI, datacenters en EV’s. Axcelis heeft de juiste technologie in huis om dit momentum te benutten.

Risico’s

- China-afhankelijkheid: >55% van de omzet komt uit China, wat risico’s geeft bij exportbeperkingen.

- Cyclische schommelingen: Q2 2025 omzetdaling van 24,2% toont de kwetsbaarheid.

- Concurrentie uit China: margedruk door opkomende lokale spelers.

- Marktvolatiliteit: beta van 1,58 maakt het aandeel gevoelig voor brede marktschommelingen.

- EV-markt: mogelijke vertraging door afnemende subsidies kan SiC-groei remmen.

Schandalen of fraude

Een onderzoek toont geen aanwijzingen voor fraude, juridische problemen of schandalen. De Q2 2025 10-Q en persberichten (waaronder 9 september 2025) vermelden geen onderzoeken of rechtszaken.

Conclusie

Axcelis staat sterk gepositioneerd voor de volgende groeifase in de halfgeleiderindustrie. Met een schuldenvrije balans, een backlog van meer dan $1 miljard en technologie die wordt gebruikt door topklanten zoals SK Hynix, biedt het bedrijf stabiliteit én groeipotentieel.

De memory-markt lijkt op een kantelpunt en vanaf eind 2025 wordt een stevige opleving verwacht, met HBM als motor. Wij gaan kopen en door de memory-rebound kan het aandeel heel hard gaan (geen garanties).

🔵 English version

Axcelis Technologies

Axcelis Technologies $ACLS is a leading supplier of ion implantation equipment for the semiconductor industry. The company provides systems that are critical to the production of chips, including mature nodes, silicon carbide (SiC), and memory products such as DRAM, NAND, and high-bandwidth memory (HBM).

We are buying. Axcelis offers investors a unique opportunity to benefit from the explosive growth of the semiconductor sector, with a particular focus on the memory market.

Although the company experienced a temporary slowdown in the summer months of 2025 due to the cyclical downturn in mature nodes and memory chips, the focus is now clearly on the promising phase expected from 2026 onwards.

Structural demand from artificial intelligence, datacenters, and electric vehicles will drive this recovery, and Axcelis is in an excellent position to benefit.

Valuation and order backlog

The valuation of the stock confirms that this is an attractive entry point. With a price-to-earnings ratio of seventeen times, Axcelis trades significantly below the average of sector peers, which indicates undervaluation compared to the broader semiconductor industry.

In addition, the company holds an order backlog of more than one billion dollars, securing a large part of revenue for the coming quarters.

This gives investors not only visibility and stability, but also the reassurance that a solid foundation is in place to build future growth.

Purion Power Series+

Another decisive factor is the introduction of the Purion Power Series+, launched on September 9, 2025. This new platform is specifically designed for the production of next-generation memory and power devices, confirming Axcelis’ role as a leading supplier in a market that is becoming increasingly complex and capital-intensive.

SK Hynix

The company has also demonstrated its ability to attract world-class customers in memory production. One example is SK Hynix, which plays a central role in the development of high-bandwidth memory. The decision of such customers to adopt Axcelis’ technology highlights the strategic importance of the Purion platform and strengthens the company’s growth potential.

All together

With an exceptionally strong balance sheet of 581 million dollars in cash and no debt, we see this stock as a compelling opportunity (no guarantees). The balance sheet provides the resilience to withstand cyclical downturns and the flexibility to continue investing in research and development, new product launches, and strategic partnerships.

All of this makes Axcelis a stock at an interesting turning point. The current valuation is attractive, the financial fundamentals are solid, and demand for memory chips is on the verge of a powerful recovery.

We therefore see this as the right moment to step in, as the memory rebound will accelerate sharply. The rise will not necessarily be in a straight line, but if the current trend in memory continues, the rally could be significant.

Memory as a catalyst

The strength of Axcelis lies in its direct exposure to the fast-growing memory market, which is essential for applications in artificial intelligence, datacenters, and high-performance computing.

While total revenue is still largely supported by mature nodes and silicon carbide, the company is increasingly positioning itself toward memory.

During the second quarter 2025 earnings call on August 5, 2025, Axcelis reported that memory applications accounted for only three percent of systems revenue.

Although this seems limited, management views it as the beginning of a significant growth curve. Demand for high-bandwidth memory, a critical component for graphics processors running AI workloads, represents a major opportunity.

The Purion family is central to this. This platform provides low-energy boron implants that improve production yields for DRAM, NAND, and HBM. Axcelis emphasized that this technology is already used in production lines of leading customers, including SK Hynix, a global leader in HBM.

On September 9, 2025, Axcelis launched the Purion Power Series+, a new system that supports superjunction architectures in power devices and is also applied in memory processes.

This positions Axcelis even more strongly in this segment, just as the market prepares for a rebound.

According to the second quarter 2025 10-Q, the memory market is currently in a cyclical downturn due to overcapacity. However, management reiterated on August 5 that a strong recovery is expected from the end of 2025 onwards.

The main drivers are large-scale investments in datacenters and the explosive growth of AI applications. As a result, Axcelis expects a significant increase in memory-related orders in 2026, which will structurally broaden its revenue base.

Latest results and outlook

Second quarter 2025 (published August 5, 2025):

Revenue: 194.5 million dollars, down 24.2 percent year-on-year (compared to 256.7 million dollars in Q2 2024).

Gross margin under GAAP: 44.9 percent (non-GAAP: 45.2 percent).

Operating margin under GAAP: 14.9 percent (non-GAAP: 17.7 percent).

Earnings per share under GAAP: 0.98 dollars (non-GAAP: 1.13 dollars).

Cash position: 581 million dollars, no debt.

Guidance for the third quarter of 2025 (ending September 30, 2025):

Revenue: around 200 million dollars.

Earnings per share under GAAP: 0.87 dollars, non-GAAP: 1.00 dollar.

Outlook (August 5, 2025):

Full-year 2025 revenue: approximately 800 million dollars.

2025 seen as the cyclical bottom, with recovery in memory and silicon carbide markets expected in 2026.

Positive catalysts

Axcelis has a series of growth drivers that will take effect over the coming quarters and years. The launch of the Purion Power Series+ and the GSD Ovation ES in September 2025 highlights Axcelis’ increased innovation strength. These systems are designed to meet the strict requirements of next-generation chip architectures, allowing the company to fully capture growth in HBM and SiC.

In August 2025, Axcelis also announced a joint development program with GE Aerospace, focused on applications in electric vehicles and power electronics (6.5–10 kilovolts). Collaborations like this strengthen Axcelis’ positioning in sectors closely linked to the energy transition and electrification of transport.

The order backlog of more than one billion dollars, confirmed on August 5, 2025, provides a stable base and clear visibility for future revenue. At the same time, Axcelis strengthened its international profile by participating in SEMICON China (June 2025), where new solutions were presented to key memory customers.

Management also emphasized that from 2026 onwards, strong demand for both HBM and SiC is expected, driven by artificial intelligence, datacenters, and electric vehicles. Axcelis has the right technology in place to seize this momentum.

Risks

- Dependence on China: more than 55 percent of revenue comes from China, which brings risks related to export restrictions.

- Cyclical fluctuations: second quarter 2025 revenue decline of 24.2 percent highlights vulnerability.

- Competition from China: increasing pressure from domestic equipment suppliers may affect margins.

- Market volatility: a beta of 1.58 makes the stock sensitive to market swings.

Electric vehicle market: a slowdown due to subsidy reductions could dampen SiC growth.

Governance and controversies

A review shows no indications of fraud, legal issues, or controversies. The second quarter 2025 10-Q and press releases, including September 9, 2025, report no investigations or lawsuits.

Conclusion

Axcelis is strongly positioned for the next growth phase in the semiconductor industry. With a debt-free balance sheet, an order backlog of more than one billion dollar, and technology already used by leading customers such as SK Hynix, the company combines stability with significant growth potential.

The memory market is at an inflection point, and from late 2025 a strong rebound is expected, with HBM as the main driver. We are buying, and the memory rebound could send the stock much higher (no guarantees).

Disclaimer Aan de door ons opgestelde informatie kan op geen enkele wijze rechten worden ontleend. Alle door ons verstrekte informatie en analyses zijn geheel vrijblijvend. Alle consequenties van het op welke wijze dan ook toepassen van de informatie blijven volledig voor uw eigen rekening.

Wij aanvaarden geen aansprakelijkheid voor de mogelijke gevolgen of schade die zouden kunnen voortvloeien uit het gebruik van de door ons gepubliceerde informatie. U bent zelf eindverantwoordelijk voor de beslissingen die u neemt met betrekking tot uw beleggingen.